Non-QM loans are specialized mortgage products that fall outside the qualified mortgage rules set by the Consumer Financial Protection Bureau, and they are exactly why real estate investors need non-QM loans to grow portfolios that conventional financing cannot reach. Traditional lenders rely on W-2s and debt-to-income ratios that penalize investors with complex tax returns, multiple properties, or self-employment income. Non-QM loans replace those rigid requirements with flexible alternatives: bank statements, rental cash flow, and asset-based income. The result is a financing path built for how investors actually earn money, not how a salaried employee does.

Why real estate investors need non-QM loans

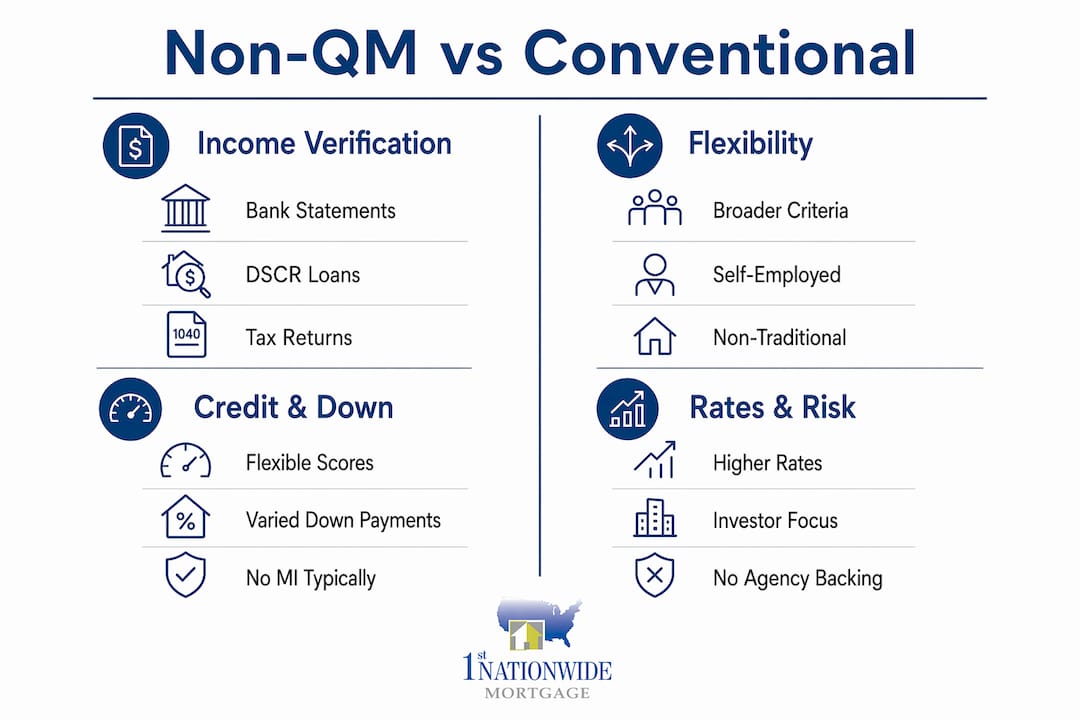

Non-QM loans are defined as mortgages that do not meet the Consumer Financial Protection Bureau’s qualified mortgage standards. Those standards require lenders to verify a borrower’s ability to repay using strict documentation, typically W-2s and tax returns. Investors who write off significant expenses often show taxable income far below their actual cash flow, which disqualifies them under conventional rules.

The core advantage is flexibility in income verification. Non-QM programs accommodate borrowers with unconventional income by using bank statements, property cash flow analysis, and 1099 earnings instead of tax returns. That flexibility is not a workaround. It is a recognition that real estate investors operate differently from salaried borrowers.

Self-employed investors face a specific problem: aggressive tax deductions reduce reported income, which tanks their debt-to-income ratio. A self-employed borrower can qualify for more than $100,000 above what a traditional tax return assessment would allow through non-QM programs. That gap represents real deals that would otherwise fall apart at the underwriting stage.

What are the key features and requirements of non-QM loans?

Non-QM loans carry distinct underwriting criteria that differ from conventional mortgages in three main areas: income documentation, credit requirements, and down payment expectations.

Income documentation methods

Bank statement loans use 12–24 months of deposits to calculate qualifying income. DSCR loans skip personal income entirely and qualify the borrower based on the property’s rental income relative to its debt obligations. Asset-based income programs count liquid assets as a proxy for monthly earnings. Each method targets a different investor profile.

Credit score and down payment requirements

Credit score requirements for non-QM loans are more flexible than conventional mortgages but still matter. A minimum score of 620 is typical for programs like bank statement loans at 1st Nationwide Mortgage. Down payments generally run higher. Non-QM loans typically require down payments of 15%–30%, compared to the median 23% seen for repeat buyers in 2025. That higher upfront requirement reflects the lender’s increased risk exposure.

Interest rates and risk profile

Non-QM loans are not backed by government agencies such as Fannie Mae or Freddie Mac. That absence of agency backing places underwriting risk directly on the lender, which drives rates higher. Investors should expect rates approximately 1%–2% above conventional mortgage rates. That premium is the cost of qualifying without traditional income documentation.

Pro Tip: Use a mortgage calculator to model the impact of a 1%–2% rate premium on your projected rental yield before committing to a non-QM loan. The math often still works in your favor when the alternative is no financing at all.

| Feature | Non-QM Loans | Conventional Loans |

|---|---|---|

| Income verification | Bank statements, DSCR, assets | W-2s and tax returns |

| Down payment | 15%–30% | 3%–20% |

| Interest rate | 1%–2% above conventional | Standard market rate |

| Agency backing | None | Fannie Mae or Freddie Mac |

| Credit minimum | Typically 620+ | Typically 620–640+ |

How do non-QM loan types differ for investors?

The major non-QM loan types include Bank Statement Loans, DSCR Loans, 1099 Loans, and NONI Loans. Each one solves a different income documentation problem.

Bank Statement Loans use 12–24 months of business or personal bank deposits to calculate qualifying income. A standard expense factor of 50% applies to business accounts, which can drop to 35%–40% with a CPA-certified profit and loss statement. These loans work best for self-employed investors whose write-offs reduce their taxable income well below actual earnings.

DSCR Loans are built specifically for real estate investors. The lender measures the property’s debt service coverage ratio, which compares rental income to the monthly mortgage payment. Qualifying based on property cash flow means your personal income never enters the equation. DSCR loans also work for LLCs and carry no limit on the number of financed properties, which makes them ideal for portfolio growth.

1099 Loans serve independent contractors and freelancers who receive 1099 income rather than W-2s. The lender uses one to two years of 1099 forms to calculate qualifying income. This product directly addresses what a non-QM loan for contractors looks like in practice: income verification without requiring tax returns that show heavy deductions.

NONI Loans (No Income, No Asset) serve foreign nationals and borrowers with no documentable income. NONI programs can reach up to $3.5 million, making them viable for high-value investment acquisitions where traditional documentation simply does not exist.

- Bank Statement Loans: best for self-employed investors with high write-offs

- DSCR Loans: best for qualifying on rental income with no personal income docs

- 1099 Loans: best for contractors and freelancers with 1099 earnings

- NONI Loans: best for foreign nationals or borrowers with no documentable income

Why do real estate investors specifically benefit from non-QM loans?

The benefits of non-QM loans for investors go beyond just qualifying. They change what deals are possible and how fast you can move on them.

-

Qualify on property income, not personal income. DSCR loans let the rental property carry its own weight. If the property generates enough cash flow to cover the mortgage, you qualify. This removes the ceiling that personal debt-to-income ratios impose on active investors.

-

Grow your portfolio without hitting a loan limit. Conventional financing caps the number of financed properties at ten. Non-QM loans carry no such restriction. Investors can finance multiple properties simultaneously, which directly supports portfolio expansion strategies.

-

Close faster on time-sensitive deals. Non-QM lenders work with alternative documentation from the start, which reduces back-and-forth during underwriting. Faster processing means you can act on off-market deals or competitive listings before other buyers.

-

Protect your personal financial profile. Qualifying through DSCR or bank statements keeps your personal tax returns and W-2 history out of the equation. That separation is valuable for investors who want to keep their business and personal finances distinct.

-

Access higher loan amounts as a self-employed borrower. Because non-QM programs use actual deposits or rental income rather than taxable income, the qualifying loan amount more accurately reflects your real financial position.

Pro Tip: If you invest in Texas, non-QM loan programs in Texas include both bank statement and DSCR options through 1st Nationwide Mortgage, which is licensed in the state and operates as a direct lender, not a broker.

What are the costs and risks of non-QM loans for investors?

Non-QM loans carry real trade-offs that every investor should weigh before committing.

- Higher interest rates reduce monthly cash flow. A 1%–2% rate premium on a $500,000 loan adds $5,000–$10,000 per year in interest costs. That affects your net operating income and cap rate calculations.

- Larger down payments increase upfront capital requirements. Higher down payments of 15%–30% tie up more equity per property, which can slow portfolio expansion if capital is limited.

- No agency backing means lenders set their own underwriting standards. Those standards vary across lenders, and terms can shift based on market conditions or the lender’s risk appetite.

- Mortgage insurance is generally not required for non-QM loans the way it is for conventional loans with less than 20% down. Lenders manage risk through higher rates and larger down payments instead. That distinction matters when you are calculating total loan costs.

- Variable lender quality is a real risk. Because non-QM loans are not standardized by agency guidelines, the quality of underwriting and loan terms depends heavily on the lender you choose.

The best way to manage these risks is to work with a direct lender, not a broker, and to run your numbers on projected rental income before applying. A deal that pencils out at a conventional rate may still work at a non-QM rate if the property cash flow is strong enough.

Key Takeaways

Non-QM loans are the most practical financing path for real estate investors who cannot qualify under conventional income documentation rules, and DSCR loans are the single most investor-specific tool in that category.

| Point | Details |

|---|---|

| Non-QM definition | Mortgages outside CFPB qualified mortgage rules, using alternative income verification. |

| DSCR loans qualify on cash flow | Property rental income replaces personal income docs, with no cap on financed properties. |

| Higher costs are the trade-off | Expect rates 1%–2% above conventional and down payments of 15%–30%. |

| Multiple loan types serve different needs | Bank Statement, DSCR, 1099, and NONI loans each target a distinct investor profile. |

| No agency backing shifts risk | Lenders set their own standards, so lender quality and terms vary significantly. |

What I’ve learned after years of non-QM lending

I have worked with real estate investors long enough to see a clear pattern. The investors who struggle with non-QM financing are almost always the ones who approach it like a conventional loan with looser rules. It is not that. It is a fundamentally different underwriting philosophy.

The biggest mistake I see is investors applying for a DSCR loan on a property with weak rental income projections, assuming the flexible documentation will compensate. It will not. The property still has to carry the debt. If the rent does not cover the payment at a reasonable coverage ratio, the loan does not close. Flexibility in documentation does not mean flexibility in math.

The second mistake is ignoring the rate premium until it is too late. A 1%–2% higher rate sounds manageable in the abstract, but on a $700,000 investment property, that is real money every month. Run the numbers before you apply, not after you are under contract.

What I find genuinely encouraging about the non-QM market in 2026 is that lender competition has improved product quality. Investors today have access to cleaner loan structures, more transparent terms, and faster closings than they did five years ago. The market has matured. That is good news for anyone building a portfolio through alternative financing.

My honest advice: use non-QM financing as a deliberate tool, not a fallback. If DSCR fits your deal, use it because it fits, not because you ran out of conventional options.

— Chris Arco, NMLS #1281

Non-QM financing options at 1st Nationwide Mortgage

Real estate investors who need flexible financing have direct access to non-QM programs through 1st Nationwide Mortgage, a direct mortgage banker licensed in 18 states and rated BBB A+.

1st Nationwide Mortgage offers DSCR loans for investors that qualify on rental income with no personal income documentation required, and bank statement loan programs that use 12–24 months of deposits for self-employed borrowers. Both programs work for LLCs and carry no limit on financed properties. If you are ready to run the numbers on your next acquisition, the investment property mortgage page at 1st Nationwide Mortgage is the right starting point. Speak directly with a licensed loan officer who understands how investors qualify, not just how salaried borrowers do.

FAQ

What is a non-QM loan?

A non-QM loan is a mortgage that does not meet the Consumer Financial Protection Bureau’s qualified mortgage standards. It uses alternative income verification methods such as bank statements, rental cash flow, or 1099 earnings instead of W-2s and tax returns.

What is the role of credit score in non-QM loans?

Credit score still matters in non-QM underwriting, with most programs requiring a minimum score of 620. A higher score can improve your rate, but non-QM lenders weigh income documentation and property cash flow alongside credit history.

Do non-QM loans require mortgage insurance?

Non-QM loans generally do not require mortgage insurance the way conventional loans do for borrowers with less than 20% down. Lenders manage their risk through higher interest rates and larger down payment requirements instead.

What is a non-QM loan for contractors?

A non-QM loan for contractors is typically a 1099 loan that uses one to two years of 1099 income forms to calculate qualifying income. It eliminates the need for tax returns that often show deductions reducing a contractor’s apparent income below what lenders would accept.

Are non-QM loans available in Texas?

Yes, non-QM loans including bank statement and DSCR programs are available in Texas through lenders like 1st Nationwide Mortgage, which is licensed in the state and operates as a direct lender.